Savings Rate (Part 1): Where Did ‘Save 10%’ Come From?

The math behind one of the most repeated pieces of financial advice

You were probably told to save at least 10% of your income for retirement somewhere along the way. More recently that number has crept up to 15%, sometimes 20%. It’s in the onboarding packet, the retirement calculator, the article your bank emails you. It’s one of the most repeated pieces of financial advice there is.

Whoever told you had a point but they didn’t have the whole picture. At best they handed you a starting point, a target, a benchmark to measure against. There’s just too much they couldn’t know: your trajectory, your priorities, how long you’ll live.

I don’t know those things about you either, and I won’t pretend to. That said, I do think it’s worth understanding where that number came from, because once you see what it was built to do, you can tell whether it was built for you.

Where You Heard It

The “save at least 10%” idea probably reached you through a parent, a teacher, or an HR rep handing out forms. Maybe an article about how unprepared most people are for retirement.

I remember filling out the 401(k) contribution line at my first accounting job. I marked 3%. A coworker who started the same week marked 10%. He was about ten years older, and when it came up, he gently pushed back on my number and suggested I make it more of a priority. He wasn’t trying to make me feel bad. He was passing along the same guidance someone had probably once handed him.

For me, that’s exactly what it did. It planted a seed. I left my contribution at 3% for the moment, and made a plan to raise it by at least a percentage point every year. The number itself mattered less than the nudge to start thinking long-term about where my money was going.

Why the Number Holds Up

The math behind 10% makes sense, for a particular set of assumptions.

Picture someone who starts working in their early 20s and plans to retire around 65, a career of 40 to 45 years. They likely won’t need to replace all of their pre-retirement income, since payroll taxes, retirement contributions, and the costs of working all fall away. Most planning lands on replacing 70 to 80% of pre-retirement income, with Social Security covering part of that and personal savings filling the rest.

Run those inputs over four decades of compounding, and a savings rate around 10% works for a lot of people. It’s the answer to a specific, reasonable question: how much do you need to save over a typical career to retire at 65 on something close to your current lifestyle?

Every Savings Rate Buys a Different Timeline

A savings rate isn't just a percentage of income. It's one of the biggest inputs determining how long you'll need to work.

One way to see this is to stop thinking about savings rate as a percentage and start thinking about it as time.

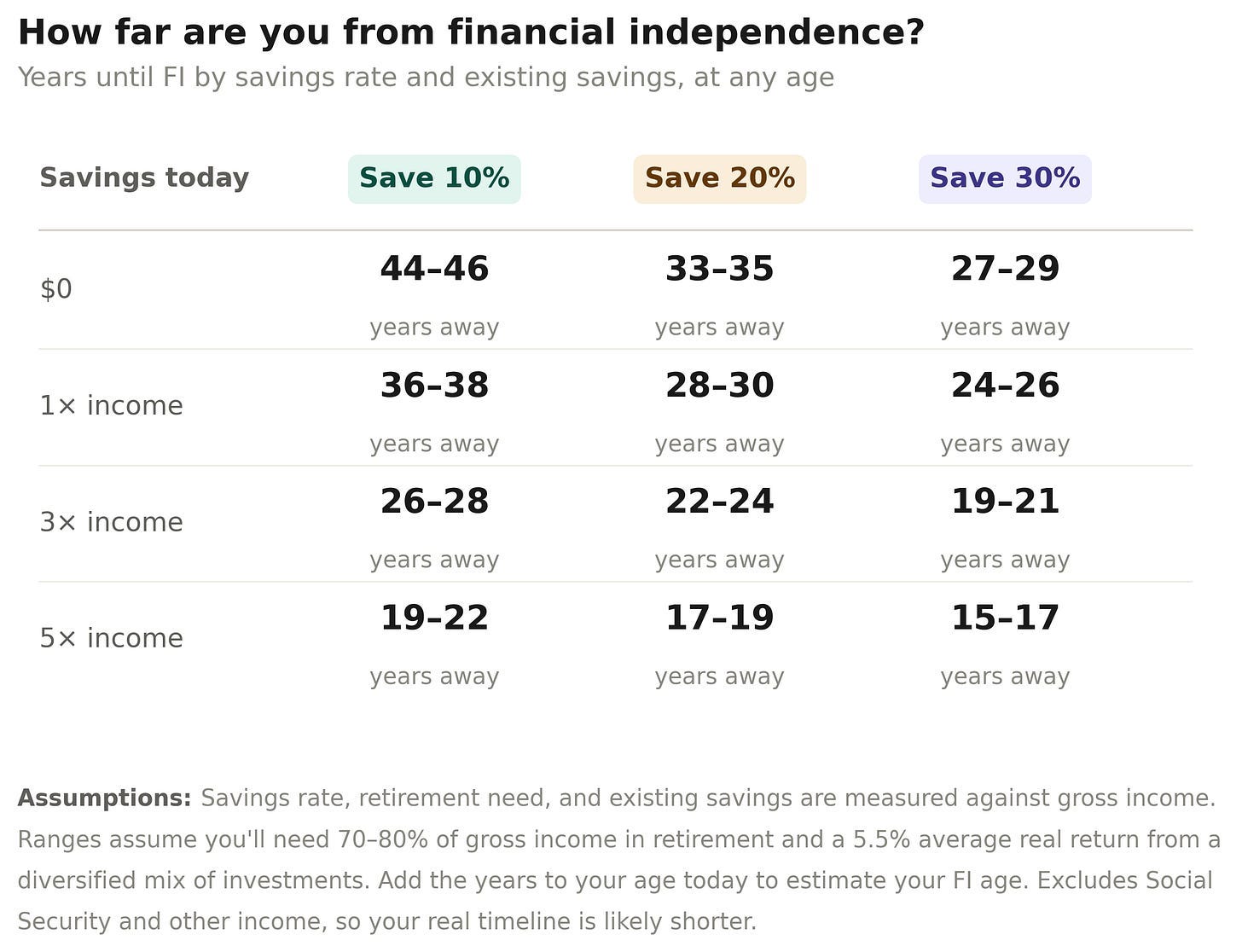

The chart below shows how long it takes to reach financial independence (FI) at different savings rates and starting portfolio sizes.

Start from zero and save 10%, and you can reach FI in about 44 to 46 years, roughly age 66 to 68 for a 22-year-old. Save 20% instead, and that drops to 33 to 35 years. That same 22-year-old could retire in their mid-to-late 50s. (An exit that early may need more than 70 to 80% replacement to bridge health insurance before Medicare, so treat the earliest numbers as a demonstration of the rate’s power more than a finished plan.)

This is why the guidance became standard: for someone who starts early and wants a traditional retirement, 10% genuinely works. Aiming for somewhere between 10-15% provides a little extra cushion for someone with a long time horizon to help if things don’t go as planned.

What About Those Starting Later

Most of us aren’t 22 anymore and likely didn’t save as much as we wish we had.

Fortunately, most of us aren’t starting from zero either.

The chart shows how much of a difference an existing portfolio makes. Someone saving 10% with 3× income already invested reaches FI roughly a decade sooner than someone starting with only 1× income.

Same savings rate. Different starting point. Different outcome.

That’s why late starters often need a higher savings rate than the traditional benchmark.

When the Question Changes

My dad once told me that during the years he was putting money away for me and my siblings’ college funds, there were stretches where our accounts held more than his own savings did. He couldn’t put as much toward his retirement then, because he was funding a different goal he cared about. He made up ground later. The point is that a lower rate at one point or another isn’t necessarily a failure. Sometimes it’s the right call for the life you’re living.

My own savings started slow. The 3% in my 401(k), a little toward an emergency fund, some other savings. My overall rate sat between 5-10% for a while, inching up each year.

It was a reasonable plan. Then I started wanting the option to stop working before my 60s while keeping the retirement my wife and I were already working toward.

That single change, pulling the date earlier, is what moved the math. If I’d planned to work longer, 10-15% would likely have funded the retirement I’m aiming for now. The driver was timing. I wanted the same kind of retirement, just sooner.

So I raised my rate. I kept increasing it each year, setting aside a portion of every raise and bonus so at least some of it went to long-term savings. That approach let my wife and me double our savings rate over each of the last two decades, helped along by careers that brought steady pay increases. Not everyone is in that position.

Here’s the part I have to stay honest about. The goalposts move. As a target comes within reach, there’s a pull to stretch further. When something becomes achievable, we tend to want a little more.

I’ve bumped up my retirement budget here and there. I weigh that increase against my current savings rate to determine if the tradeoff of needing to save more makes sense. For now, the balance between living today and funding tomorrow feels close to right. But I expect to keep revisiting it.

Rules of Thumb Are Answers. Check the Question.

The 10-15% guidance is an answer, and sometimes a good one, to a question you may or may not be asking.

Most financial rules of thumb work this way. Someone ran a calculation with reasonable assumptions and compressed the result into a number you could remember. Save 10% for retirement. Keep three to six months of expenses on hand for emergencies. Withdraw 4% a year in retirement so your money will last. These are all useful pieces of advice but might not always line up perfectly with your own FI equation. That’s why it’s worth the time to understand them and make some adjustments before you build a life around them.

You don’t have to settle your retirement vision today. It will move. Mine did and probably will again. What you have now is the ability to check, whenever you want, whether your pace and your destination still belong to the same plan. Most people never get that far.

Checking starts with a number: your own savings rate, measured the same way throughout this series, and what it’s actually doing for you. That’s Part 2.

— Brad

New here? Start here.

Or read more at The FI Equation.

If this way of thinking about financial independence resonates, subscribe for free to get future posts emailed each week.

This is meant to help you think through financial decisions and tradeoffs—not tell you exactly what to do. It’s general in nature and not personalized advice (see full disclaimer).